The Hidden Downsides Of Claiming Social Security At Age 70

Similar to the advice of not using credit cards or making extra mortgage payments, waiting as long as possible to begin collecting social security is a popular recommendation amongst some personal finance experts. However, also like those other bits of advice, waiting until 70 years old to begin collecting social security isn't a one-size-fits-all approach. In fact there are numerous downsides to consider.

What financial experts do have correct is that you'll receive a larger monthly payment by waiting to begin collecting your social security. Retirees can currently start receiving benefits as early as age 62. That said, the Social Security Administration (SSA) considers the full retirement age to be between 66 and 67 years old, depending on when exactly you were born. For Americans born in 1960 or later, full retirement age is 67. In 2024, a retiree who starts taking benefits at age 62 will receive approximately 30% smaller monthly payments than if they wait to receive full benefits at age 67.

Retirees who delay until after full retirement age to begin taking benefits can actually earn an amount that's greater than full benefits. According to the SSA, "We'll add 8% to your benefit for each full year you delay receiving Social Security benefits beyond full retirement age." To be clear, that offer extends until a retiree reaches age 70. Clearly, waiting until 70 will result in larger monthly checks, so what are the downsides? Let's investigate.

Life expectancy is a consideration

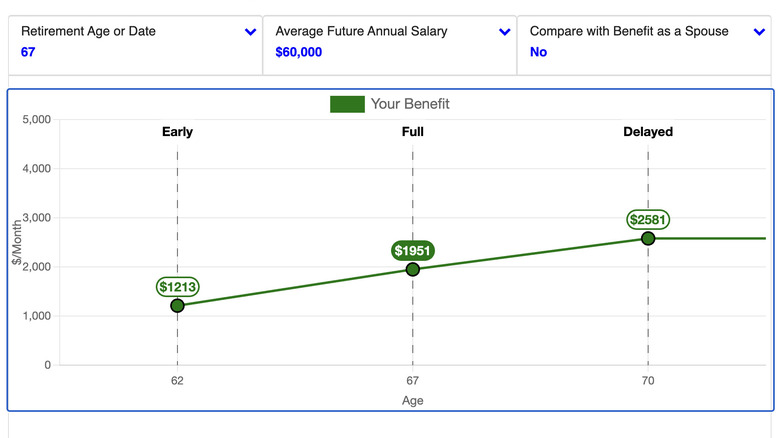

The most obvious hazard to waiting to receive social security payments is if you die earlier than expected. Although the reward for waiting until 70 is a larger payment, it will take a number of years to overtake the aggregate amount of dollars received if starting earlier in your 60s.

For instance, referencing the above chart pulled from the SSA website, a retiree collecting $2,581 per month for five years (age 70 to 75) would receive a total of $154,860 ($2,581 * 60 months). On the other hand, receiving $1,213 for 13 years between age 62 and 75 would result in a total of $189,228 ($1,213 * 156 months). Of course, predicting one's demise is a difficult and macabre business, but known health issues or family history might help to make a rough guess whether you're better to begin collecting benefits sooner than later.

As well, retirees need to consider that social security benefits don't pass down to next of kin. While social security can be collected by a spouse under certain circumstances, you can forget about your children or grandchildren receiving any of your hard-earned benefits. That's as opposed to a savings account, brokerage account, or retirement accounts like an IRA or 401(k) that can be passed along to beneficiaries. Therefore, if you're spending savings and/or taking retirement account withdrawals in your 60s in order to max out social security payments, know that this practice could result in a smaller financial legacy to pass down to loved ones.

Couples should tackle social security as a team

Finally, retirees must consider spousal benefits when determining the optimum time to start receiving social security payments. For example, a lower earning spouse is eligible to receive up to half of the higher earning spouse's benefits as calculated at that person's full retirement age, not at age 70. Still, half of the higher earner's benefits may be more than the lower earner is entitle to on his or her own. Hence, that's an incentive for the lower earning partner to begin benefits sooner rather than later.

To be clear, couples can take advantage of the above spousal benefits while both individuals are still living. On the other hand, survivor benefits occur when one spouse passes away. The surviving spouse is entitled to the same amount of social security that their partner was receiving, assuming that number was higher for the deceased. In general, if both halves of a couple are collecting social security, it makes more sense for the lower earning spouse to start collecting earlier, while the higher earner holds out for larger monthly payments.

To summarize, you should consider your overall health, strategy as a couple, and bequeathment goals when deciding if you should wait until 70 — or even 66 or 67 — years old to start collecting on your social security benefits. It could also be worth consulting with a personal finance or investment professional to review this complicated topic. Just be sure to choose a financial advisor wisely, not one who applies blanket advice to more nuanced decisions.