The Most Important Financial Skill For People Entering The Workforce Later In Life

Entering, or reentering, the workforce later in life can feel daunting. Between new technologies, terminologies, and workplace cultural attitudes, it can be easy to feel overwhelmed. Yet, perhaps one of the most difficult things about this new chapter in your life can be the financials. Whether you've traditionally had two incomes or were someone who could afford and/or chose not to work, entering the workforce later in life could also be a result of a host of other personal life changes. Chances are that financial changes are at least part of your new situation and learning to navigate those changes can be challenging, not to mention confusing.

We spoke with Lawrence Sprung, CFP, author of "Financial Planning Made Personal," and Founder of Mitlin Financial about the best financial tips and skills for those entering the workforce later in life. You might be surprised to learn his No. 1 priority was budgeting. While you could be thinking you know what a budget is, implementing one can be a different story. Consider, according to a 2023 NerdWallet survey, even though 74% of Americans reported having a monthly budget, the number trended downward by generation, with only 67% of baby boomers reporting keeping such a budget themselves.

Plus, NerdWallet found that 84% reported exceeding their monthly budget. Also interesting is that only 13% of boomers and 26% of Generation Xers reported they needed a budget to manage their finances. However, the biggest category for overspending wasn't something like online shopping or entertainment, it was food, namely groceries, which have experienced a 29% price increase since 2020.

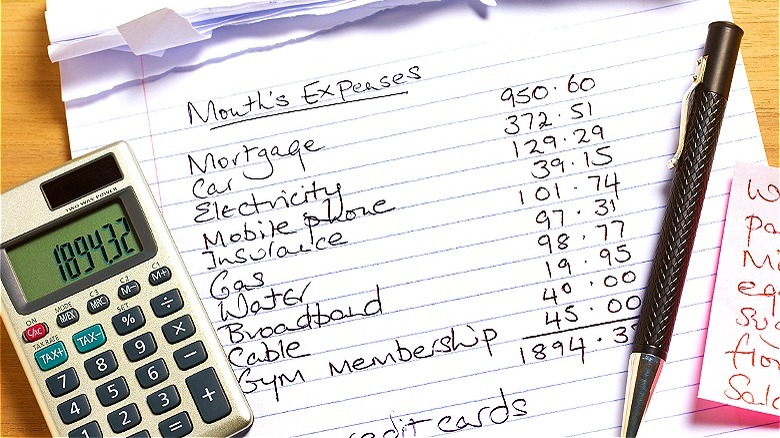

Budgeting

While it might sound simple enough, budgeting can prove an extremely foundational part of your finances. Yet, how you view budgeting is essential to your success. As Lawrence Sprung explained, "Budgeting is not about expense shaming; budgeting is about understanding money in and money out and getting a handle on whether your current spending and savings levels will allow you to meet your goals." This can apply to any financial goals you might have, whether it's saving up for a large purchase like a car (but make sure you pay attention to when, exactly, you buy a new car), building up an emergency fund, or even paying down debt. Budgeting can help you balance your present financial obligations with your future financial goals.

Another important consideration for those entering the workforce later in life is that time isn't necessarily on your side when it comes to personal finances. "A person in their 50s who has never worked before will have to make sure that they are doing everything they can to be on track toward their goals," said Sprung. "Unlike someone in their 20s, they do not have the time to recover from making a significant misstep in their financial life." Savings goals can be especially difficult when starting later in life, especially in the face of current debt levels in the U.S. For instance, the total household debt in the United States currently stands at $17.69 trillion, with 28% of Americans reporting having less than $1,000 in their savings, according to Forbes.

Pitfalls of budget rules

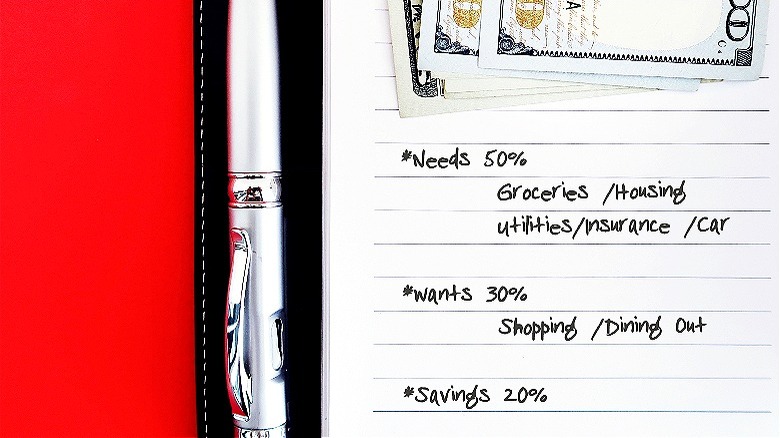

Keep in mind that there are a LOT of different budget rules out there, and it can be easy to think following one of them will simplify your life. However, increasingly, these budget rules do not fit current economic circumstances. As these kinds of budget rules get increasingly less realistic, it can be financially dangerous to try and force your budget to fit their specifications. For example, the 50/30/20 budget rule is a popular (if unrealistic) choice for many people, laying out that 50% of your monthly expenses should go to things you need, 30% to your wants, and 20% to savings. While, in general, the premise of these budget rules is positive, they often miss things like the rapid increase in car prices, housing, and interest rates. These changes can push certain expense categories far and away above what a budget rule might consider "normal" or ideal.

The biggest thing to keep in mind is picking a budget type that ultimately works for you and your financial situation, regardless of its popularity. It's also important to hold yourself accountable to that budget, which means regularly checking in on your expenses and ensuring you're meeting specific goals every month. While tracking your spending might not be the most exciting way to spend your time, remember that there are plenty of tools to help. From budget calculators to tracking apps, it's easier than ever to monitor spending and make sure it lines up with the income from your new job.